How many credit cards should I have in the UK? Discover the ideal number for your credit score, debt control, and long-term financial stability.

Some people worry they have too many cards. Others worry they do not have enough to build a good credit score. The truth is there is no single “correct” number. The right number of credit cards depends on how you use them, how well you track spending, and how stable your finances are.

This guide explains how many credit cards most people in the UK can manage safely, what actually matters more than the number, and how to decide what is right for you.

Is There a Recommended Number of Credit Cards in the UK?

There is no official recommended number of credit cards in the UK. Lenders and credit reference agencies do not set a limit.

Instead, they look at how responsibly you manage the credit you already have.

That means:

- Paying on time

- Keeping balances under control

- Avoiding heavy reliance on credit

- Showing consistency over time

Someone with one well-managed credit card can look lower risk than someone with five cards that are poorly managed. The number itself is not the main issue.

How Many Credit Cards Do Most UK Adults Have?

UK data consistently shows that most adults with credit cards have between one and three cards.

For many people:

- One card is enough for everyday spending

- Two cards allow separation of spending types

- Three cards may cover rewards, balance transfers, or emergencies

Problems tend to increase when cards are added without a clear purpose.

If you are asking “how many credit cards should I have UK”, the safer range for most households is usually one to two cards, especially if you are budgeting or paying down debt.

When Having More Than One Credit Card Can Make Sense

Having more than one credit card is not automatically a bad thing.

Multiple cards can be useful if:

- You separate everyday spending from large purchases

- One card is used for rewards and is paid in full

- One card is reserved for emergencies only

- You are managing a temporary balance transfer

In these cases, each card has a defined role. That clarity matters more than the number.

Using this approach fits well with the wider principles explained in Credit Cards and Debt Explained for UK Families, where structure and visibility are key.

When Too Many Credit Cards Become a Problem

Issues usually start when cards are added without intention.

Warning signs include:

- Losing track of balances

- Only paying minimum payments

- Using cards interchangeably

- Feeling anxious about statements

- Relying on credit to cover shortfalls

At that point, the question is no longer “how many credit cards should I have UK” but whether credit card use is supporting or undermining your finances.

If cards are making budgeting harder, this is closely linked to the issues discussed in Are Credit Cards Bad for Budgeting?

Does Having More Credit Cards Improve Your Credit Score?

This is a common misconception.

Having more credit cards does not automatically improve your credit score.

What matters is:

- Payment history

- Credit utilisation

- Length of credit history

- Stability of accounts

One well-managed card can build credit just as effectively as several cards. In some cases, opening too many cards can temporarily lower your score due to hard credit checks.

Quality of use always matters more than quantity.

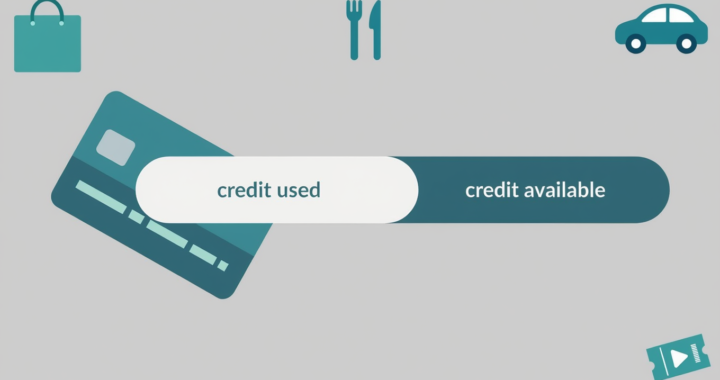

Credit Card Utilisation Matters More Than Card Count

Credit utilisation refers to how much of your available credit you are using.

For example:

- £1,000 balance on a £5,000 limit equals 20 percent utilisation

- £1,000 balance on a £1,500 limit equals 67 percent utilisation

Lower utilisation generally looks healthier.

Sometimes people open additional cards to increase their total available credit and lower utilisation. This can help, but only if spending stays controlled.

If spending increases alongside new cards, utilisation problems remain. This is explained in more detail in Credit Card Utilisation Explained (UK).

How Many Credit Cards Should a Family Have?

For families, simplicity usually wins.

Most families function best with:

- One main spending card

- Optional second card for emergencies or specific purposes

More cards mean:

- More statements

- More tracking

- More risk of missed payments

If you are managing household finances, fewer cards often mean clearer budgeting and less stress.

This fits into the broader guidance in Credit Cards and Debt Explained for UK Families, where visibility and consistency matter more than optimisation.

Should You Close Unused Credit Cards?

Closing a credit card is not always necessary, but it can be helpful in some cases.

You might consider closing a card if:

- You no longer use it

- It tempts overspending

- It adds mental clutter

However, closing older cards can shorten your credit history. A common approach is to keep older, unused cards open with zero balance, as long as they do not encourage spending.

There is no need to rush this decision. The goal is control, not perfection.

A Simple Way to Decide How Many Credit Cards You Should Have

Ask yourself three questions:

- Can I name the purpose of each card?

- Can I check all balances without stress?

- Am I paying off spending in a way that reduces debt over time?

If the answer is yes, your number of cards is probably fine.

If the answer is no, reducing the number of cards may bring clarity faster than adding more.

Frequently Asked Questions About How Many Credit Cards You Should Have in the UK

How many credit cards should you have in the UK?

There is no single correct number of credit cards. Many people in the UK have between one and three cards, depending on their financial situation.

The important factor is not the number of cards, but whether they are managed responsibly with on time payments and low balances.

Is it bad to have multiple credit cards?

Having multiple credit cards is not automatically bad.

In some cases, having more than one card can actually help your credit profile by increasing your total available credit and improving your credit utilisation ratio. Problems usually arise when balances become difficult to manage.

Can having more credit cards improve your credit score?

Sometimes it can.

If additional cards increase your available credit while balances remain low, your credit utilisation ratio may improve, which can support your credit score.

However, opening too many cards in a short time can temporarily lower your score because of multiple credit checks.

Is it better to have one credit card or several?

Both approaches can work.

One card keeps things simple and easier to manage. Several cards may offer benefits such as spreading spending, separating budgets, or increasing available credit.

The best approach is the one that fits your spending habits and financial discipline.

How many credit card applications are too many?

Applying for several credit cards in a short period can lower your credit score temporarily.

Lenders may see multiple applications as a sign that someone urgently needs credit. Spacing applications out over time usually creates a healthier credit profile.

Does having too many credit cards hurt your credit score?

Simply having multiple cards does not usually harm your credit score.

What matters is how the cards are used. High balances, missed payments, or frequent applications are far more important factors than the total number of cards.

Should I close credit cards I do not use?

Not always.

Closing unused cards can reduce your available credit and increase your utilisation ratio. It can also shorten your credit history if the account is old.

If a card has no annual fee and does not encourage spending, keeping it open with a zero balance may be beneficial.

Can you have too much available credit?

Large amounts of available credit are not necessarily a problem if spending remains controlled.

However, lenders may review total available credit when assessing new applications, particularly for loans or mortgages.

Is having three credit cards too many?

For many people, three credit cards is a manageable number.

Some people use one card for everyday spending, another for purchases or rewards, and another as a backup. The key is making sure all cards are included in your budget and payments are always made on time.

What matters more than the number of credit cards?

Credit scoring systems focus more on behaviour over time rather than the number of accounts.

Important factors include:

• Paying on time every month

• Keeping balances low compared to limits

• Avoiding frequent credit applications

• Managing credit consistently

These habits have a much greater influence on your credit profile than the exact number of cards you hold.

Final Thoughts

If you are searching for “how many credit cards should I have UK”, the honest answer is this:

You should have as many credit cards as you can manage clearly, and no more.

For most people, that is one or two.

For some, it may be three.

For many families, fewer cards mean better control.

Credit cards are tools. The right number is the one that supports your financial stability, not the one that looks optimal on paper.

For a full overview of how card numbers, balances, and habits fit together, see Credit Cards and Debt Explained for UK Families.

Related Credit Card Guides

If you are working to improve your finances, these guides can also help:

• Learn what really happens when you only pay the minimum on a credit card

https://budgetkin.com/paying-the-minimum-on-a-credit-card-what-really-happens-in-the-uk/

• Understand how credit card utilisation affects your credit score

https://budgetkin.com/credit-card-utilisation-explained-and-why-it-matters-in-the-uk/

• Avoid credit card mistakes that hurt your finances

https://budgetkin.com/credit-card-mistakes-that-hurt-your-finances/

• Explore proven debt repayment strategies to crush your debt

https://budgetkin.com/proven-debt-repayment-strategies-to-crush-your-debt/

Pingback: Credit Card Utilisation Explained (And Why It Matters in the UK) - BudgetKin

Pingback: Credit Card Mistakes That Hurt Your Credit Score in the UK - BudgetKin