Credit card utilisation is one of the most misunderstood parts of personal finance in the UK. Many people have credit cards, pay on time, and still see their credit score struggle without knowing why.

If you are trying to use credit cards responsibly, reduce debt, or improve your credit profile, understanding utilisation is essential. This guide explains what credit card utilisation is, how it works in the UK, and how to manage it without overthinking your finances.

What Is Credit Card Utilisation?

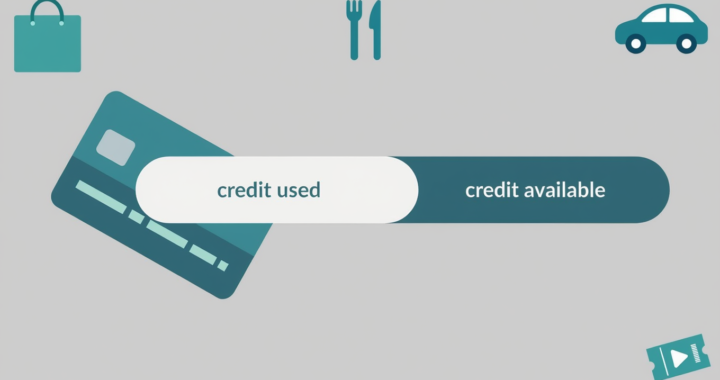

Credit card utilisation is the percentage of your available credit that you are currently using.

It is calculated by dividing your balance by your credit limit.

For example:

- £500 balance on a £5,000 limit = 10 percent utilisation

- £2,500 balance on a £5,000 limit = 50 percent utilisation

This applies:

- Per individual card

- Across all your credit cards combined

Both matter.

Why Credit Card Utilisation Matters in the UK

Credit reference agencies in the UK look at utilisation because it shows how dependent you are on credit.

High utilisation can suggest:

- Financial pressure

- Heavy reliance on borrowing

- Higher risk to lenders

Low utilisation suggests:

- Controlled spending

- Capacity to manage credit

- Lower perceived risk

This is why utilisation often affects credit scores even when payments are always made on time.

What Is a Good Credit Card Utilisation Percentage?

There is no official rule, but widely accepted guidance in the UK suggests:

- Under 30 percent is generally considered healthy

- Under 25 percent is even better

- Over 50 percent may raise concern

- Near or at 100 percent is a red flag

These are not hard limits. They are risk signals.

Someone consistently using 80 percent of their credit limit may struggle to improve their credit profile, even with perfect payment history.

Credit Card Utilisation Per Card vs Overall

This is where many people get caught out.

Example:

- Card A: £900 balance on £1,000 limit, 90 percent utilisation

- Card B: £100 balance on £4,000 limit, 2.5 percent utilisation

Overall utilisation is low, but one card is maxed out.

Lenders often look at both:

- Individual card utilisation

- Total utilisation across all cards

Maxing out one card can still be a negative signal, even if overall usage looks reasonable.

Does High Utilisation Mean You Are Bad With Money?

No. High utilisation does not automatically mean poor money management.

High utilisation often happens because:

- Limits are low

- Income is stretched temporarily

- Cards are used to smooth cash flow

- Spending is essential, not reckless

However, if high utilisation becomes the norm, it increases stress and makes debt harder to reduce.

This is why utilisation fits into the broader framework explained in Credit Cards and Debt Explained for UK Families.

How Credit Card Utilisation Affects Budgeting

Utilisation and budgeting are closely linked.

When utilisation is high:

- Credit card balances feel heavy

- Minimum payments increase

- Budgets become tighter

- Stress increases

This is one reason some people feel that credit cards break budgets. The issue is not the card itself, but the level of reliance on credit.

This relationship is explored further in Are Credit Cards Bad for Budgeting?

Should You Open Another Credit Card to Lower Utilisation?

Sometimes people consider opening a new card to increase their total available credit and lower utilisation.

This can work only if:

- Spending stays the same

- New credit is not used to spend more

- You can manage another account

Opening a new card also creates a hard credit check, which may temporarily affect your score.

If the new card leads to higher spending, utilisation problems usually return quickly.

How to Lower Credit Card Utilisation Safely

Practical ways to reduce utilisation include:

- Paying down balances steadily

- Making extra payments mid-month

- Avoiding maxing out any single card

- Keeping spending within budgeted categories

Lowering utilisation does not require perfection. Even small reductions can improve clarity and reduce stress.

Paying down balances quickly is one of the best ways to improve utilisation and your credit score. These debt repayment strategies can help accelerate that process.

If you are unsure how many cards you should manage while doing this, see How Many Credit Cards Should I Have in the UK?

Credit Card Utilisation for Families

For families, utilisation can rise quickly due to shared expenses and irregular costs.

Helpful approaches include:

- Using one main card for tracked spending

- Avoiding multiple cards carrying balances

- Reviewing balances weekly

- Planning for irregular costs in advance

Lower utilisation often brings immediate emotional relief, not just technical credit improvements.

Does Credit Card Utilisation Reset Every Month?

Utilisation is not fixed permanently.

It changes as:

- Balances change

- Statements are generated

- Payments are made

This means improvement is possible without closing accounts or drastic changes. Consistency matters more than one perfect month.

Frequently Asked Questions About Credit Card Utilisation

What is credit card utilisation?

Credit card utilisation is the percentage of your available credit that you are currently using.

For example, if your credit card limit is £1,000 and your balance is £300, your utilisation is 30 percent.

Lenders and credit scoring systems use this number to understand how much of your available credit you rely on.

What is a good credit utilisation ratio?

Most credit experts suggest keeping utilisation below 30 percent.

Lower is generally better. Many people with excellent credit scores keep their utilisation below 10 percent.

However, the key point is not to regularly use most of your available credit.

Does credit utilisation affect your credit score?

Yes. Credit utilisation is one of the most important factors in credit scoring.

If you use a high percentage of your credit limit, lenders may see that as a higher risk, even if you always make payments on time.

Keeping balances low compared to your limit can help maintain a healthier credit profile.

Is 50 percent credit utilisation bad?

Using around 50 percent of your credit limit is not automatically a problem, but it can start to reduce your credit score.

Many credit scoring models view utilisation above 30 percent as a sign that someone may be relying too heavily on credit.

Does paying off your credit card reduce utilisation immediately?

Yes. When your balance drops, your utilisation ratio also drops.

However, credit reports usually update after the lender sends a monthly statement update. This means the change may take a few weeks to appear on your credit file.

Is it better to have multiple credit cards for utilisation?

Sometimes having more than one card can help reduce your overall utilisation because your total available credit increases.

However, this only helps if you keep balances low. Opening new cards just to increase limits is not always the right solution.

Does credit utilisation reset every month?

Your utilisation changes whenever your balance changes.

However, most credit reports reflect the balance that appears on your statement date, not necessarily the balance after you make a payment.

This is why some people choose to pay part of their balance before the statement is generated.

Can high credit utilisation damage your credit score quickly?

Yes, it can.

If your balances suddenly increase and your utilisation jumps above 50 percent or 75 percent, your credit score may drop temporarily.

The good news is that utilisation also recovers quickly once balances are reduced.

Should I keep a small balance on my credit card for my credit score?

No. This is a common myth.

You do not need to carry a balance to build credit. Paying your balance in full each month is usually the best financial approach and still helps build a positive credit history.

What is the easiest way to keep credit utilisation low?

Some practical strategies include:

• Paying part of your balance before the statement date

• Spreading spending across multiple cards

• Requesting a credit limit increase if appropriate

• Avoiding maxing out a single card

The most effective approach is simply keeping balances low compared to the limit.

Final Thoughts

If you are searching for “credit card utilisation explained UK”, the key takeaway is this:

Credit card utilisation is not about how many cards you have.

It is about how much of your available credit you rely on.

Lower utilisation usually means:

- Less stress

- More control

- Better long-term outcomes

Understanding this concept makes it much easier to use credit cards responsibly and avoid unnecessary debt.

For a complete view of how utilisation fits into everyday spending, debt, and budgeting, read Credit Cards and Debt Explained for UK Families.

Related Credit Card Guides

If you are working to improve your finances, these guides can also help:

• Understand how credit card utilisation affects your credit score

https://budgetkin.com/credit-card-utilisation-explained-and-why-it-matters-in-the-uk/

• Learn what really happens when you only pay the minimum on a credit card

https://budgetkin.com/paying-the-minimum-on-a-credit-card-what-really-happens-in-the-uk/

• Avoid credit card mistakes that hurt your finances

https://budgetkin.com/credit-card-mistakes-that-hurt-your-finances/

• Explore proven debt repayment strategies to crush your debt

https://budgetkin.com/proven-debt-repayment-strategies-to-crush-your-debt/

Pingback: Should I Pay My Credit Card in Full Every Month? - BudgetKin

Pingback: 10 Proven Debt Repayment Strategies to Crush Your Debt - BudgetKin

Pingback: Credit Card Mistakes That Hurt Your Credit Score in the UK - BudgetKin