Master Hybrid Budgeting to manage variable income with confidence. Learn how to blend zero-based and envelope budgeting for flexible, stress-free finances that fit your gig or freelance lifestyle.

Hybrid Budgeting: The Smart Way to Manage Variable Income

When I started freelancing, I felt like my income was a roller coaster. One month I earned plenty, the next I barely covered rent. I tried spreadsheets, tracking apps, and traditional monthly budgets, but none worked. Everything changed when I discovered Hybrid Budgeting, a simple and realistic way to manage irregular income without stress.

Hybrid Budgeting is not about being perfect with money. It is about being consistent and intentional. Whether you are a freelancer, gig worker, contractor, or seasonal employee, this system helps you stay organized even when your income is unpredictable.

What Is Hybrid Budgeting?

Hybrid Budgeting blends two powerful systems, the Envelope Method and Zero-Based Budgeting. Each has unique strengths, and when combined, they form a flexible system that keeps every pound purposeful.

- The Envelope Method divides your money into categories like rent, groceries, and savings, so you always know what is available for each need.

- Zero-Based Budgeting assigns every pound a specific role until your income minus expenses equals zero. Nothing is left idle, and nothing is wasted.

Together, they create Hybrid Budgeting, a system that provides structure without rigidity. It lets you handle income fluctuations gracefully, keeping your priorities front and center.

Why Hybrid Budgeting Works for People with Variable Income

Most budgeting advice assumes your income is steady, but that is not reality for freelancers and gig workers. With Hybrid Budgeting, you gain flexibility and control.

Here is why this approach stands out:

- Flexibility built in. You can adjust envelopes month to month without breaking the plan.

- Essentials come first. You fund what matters most before discretionary spending.

- Natural spending limits. Once an envelope is empty, you stop or pause that category.

- Savings grow in strong months. You can move extra income into buffer envelopes for leaner times.

- Digital or cash friendly. Hybrid Budgeting works with modern apps or traditional envelopes.

It is a system designed for real life, not perfection.

How to Start Hybrid Budgeting Step by Step

Hybrid Budgeting can look complicated at first, but once you start, it quickly becomes second nature. Follow these simple steps.

Step 1: Calculate Your Average Monthly Income

Gather your earnings from the last 6 to 12 months. Add them up, then divide by the number of months. That gives you a realistic average to plan with.

Even if your income changes, this number helps you create a stable foundation for your budget.

Step 2: List All Expenses

Separate your fixed expenses like rent, insurance, and utilities from variable expenses like food, entertainment, or fuel.

Create envelopes for each major category. Examples include:

- Rent and Utilities

- Groceries

- Transportation

- Health and Insurance

- Savings and Buffer

- Fun or Discretionary Spending

Step 3: Prioritize Essentials First

Fund your must-have envelopes first, such as housing, bills, and food. Then, move to flexible categories like entertainment or clothing.

When income is tight, essentials always come first.

Step 4: Assign Every Pound a Job

This step is the heart of Zero-Based Budgeting. Take your total income and allocate every pound to an envelope until all funds are accounted for.

Use this formula:

Income – Expenses – Savings = 0

This ensures your money is working for you, not sitting idle or being spent mindlessly.

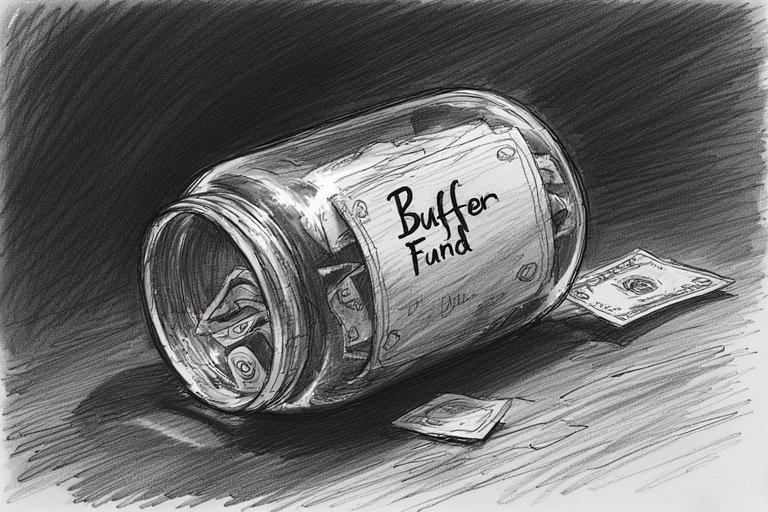

Step 5: Create a Buffer Envelope

The buffer envelope is your safety net. In good months, you add extra income here. When income dips, you draw from this fund instead of using credit cards.

According to Fidelity Investments, saving one to two months of living expenses as a buffer creates financial stability and reduces stress.

Step 6: Use Technology to Simplify

Modern budgeting tools make Hybrid Budgeting simple and effective. Consider:

- YNAB (You Need A Budget) for zero-based budgeting and progress tracking.

- Goodbudget for digital envelope management.

- Actual Budget for privacy and offline control.

These apps allow automatic updates, spending alerts, and easy visualization of your envelopes.

Example: Hybrid Budgeting in Real Life

Let me show you how Hybrid Budgeting looks in practice.

Meet Alex, a freelance web designer with an income that varies between £3,000 and £5,000 per month.

He calculates his 6-month average at £4,000 and uses that as his base. His Hybrid Budget looks like this:

| Category | Envelope Amount |

|---|---|

| Rent and Utilities | £1,200 |

| Groceries and Food | £400 |

| Transportation | £300 |

| Health and Insurance | £300 |

| Emergency Savings Buffer | £500 |

| Debt Repayment | £300 |

| Tools and Software | £200 |

| Fun and Discretionary | £100 |

| Total | £3,300 |

Alex then adds the remaining £700 into his buffer envelope for future slow months. When his income is lower, he draws from that instead of using credit.

This setup gives him confidence that his essentials are always covered, even when his income changes.

Common Mistakes to Avoid in Hybrid Budgeting

I have made all these mistakes before, and you can skip them by keeping things simple.

- Neglecting to track income. Keep accurate records of every pound you earn.

- Creating too many envelopes. Too many categories make tracking difficult. Stick to 8-12 main envelopes.

- Forgetting the buffer. The buffer is your safety cushion. Always fund it first when income is high.

- Failing to review. Check your budget every week or month. Small adjustments prevent big surprises.

- Using Hybrid Budgeting as a fixed rulebook. It is flexible by design, so adapt it to your lifestyle.

The Emotional and Practical Benefits of Hybrid Budgeting

Hybrid Budgeting is more than a financial system. It is a mindset shift that promotes confidence, security, and peace of mind.

Here are the most meaningful benefits:

- Less anxiety about money. You always know where your income goes.

- Better sleep and focus. Financial clarity reduces stress and mental clutter.

- Greater control and awareness. You make financial decisions with intention.

- Improved savings habits. You build stability even in unpredictable times.

A study by the American Psychological Association found that financial uncertainty is one of the top sources of stress. Having a clear plan like Hybrid Budgeting helps reduce that tension and supports better mental health.

Expert Support for Hybrid Budgeting

Financial experts increasingly recommend hybrid and zero-based systems for self-employed workers.

- Fidelity Investments promotes zero-based planning to ensure every dollar has purpose.

- Dave Ramsey continues to champion the envelope system as a tool for spending discipline.

- Freelancers Union advises freelancers to build cash buffers and adjust budgets monthly.

- YNAB integrates both concepts digitally, helping people manage variable income efficiently.

These organizations highlight what many of us discover through trial and error: combining structure with flexibility is the key to financial peace.

Practical Tips to Make Hybrid Budgeting Stick

If you want Hybrid Budgeting to become a habit, focus on simplicity and consistency.

- Start with only a few envelopes and add more over time.

- Review your budget once a week.

- Automate savings transfers into your buffer fund.

- Use an app that gives you visual progress tracking.

- Keep your goals visible, such as paying off debt or saving for a new project.

Once you feel confident, you can add layers like investing, retirement savings, or long-term goals.

Key Takeaways

- Hybrid Budgeting blends the Envelope Method and Zero-Based Budgeting.

- It is ideal for freelancers, gig workers, and anyone with fluctuating income.

- Every dollar has a purpose, helping you stay in control.

- A budget buffer smooths out lean months and prevents credit reliance.

- Consistent review and adjustment make this system sustainable.

Conclusion and Call to Action

If you earn irregular income, Hybrid Budgeting can change your financial life. It is flexible, simple, and realistic. You will no longer feel like you are chasing your money each month. Instead, you will have a clear plan that adapts with you.

Start by setting up your envelopes and assigning every dollar a purpose. Build your buffer fund, review regularly, and use tools that simplify your system. Within a few months, you will notice reduced stress and greater financial stability.

For practical next steps, visit:

For authoritative insights and tools, explore:

- Fidelity Investments: How to Budget for Irregular IncomeFƒ

- Dave Ramsey: The Envelope System

- YNAB: Zero-Based Budgeting Tools

Hybrid Budgeting is more than a money strategy. It is a path to calm, clarity, and long-term confidence. Start your journey today and see how much lighter financial life can feel when every dollar finally makes sense.

Pingback: 10 Sneaky Budget Busters Draining Your Family Finances - BudgetKin

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.