Paying the minimum on a credit card can keep you stuck in debt for years. Learn what really happens in the UK, how interest works, and what to do instead.

This post explains what minimum payments really do, how they affect debt and budgets, and why so many UK households get stuck even when they think they are being responsible.

What Is a Credit Card Minimum Payment?

A minimum payment is the smallest amount your credit card provider allows you to pay each month to keep your account up to date.

In the UK, minimum payments are usually calculated as:

- A percentage of your balance, often around 2 to 3 percent, or

- A fixed amount, whichever is higher

This payment is designed to keep the account active, not to clear the debt quickly.

What Happens When You Only Pay the Minimum?

When you only pay the minimum credit card payment, several things happen at once.

- Most of your payment goes toward interest

- Only a small amount reduces the balance

- The debt clears very slowly

- The total cost of borrowing increases

This is why balances can linger for years even when payments are made every month.

Understanding this behaviour is a key part of using credit cards safely, which is explained more fully in Credit Cards and Debt Explained for UK Families.

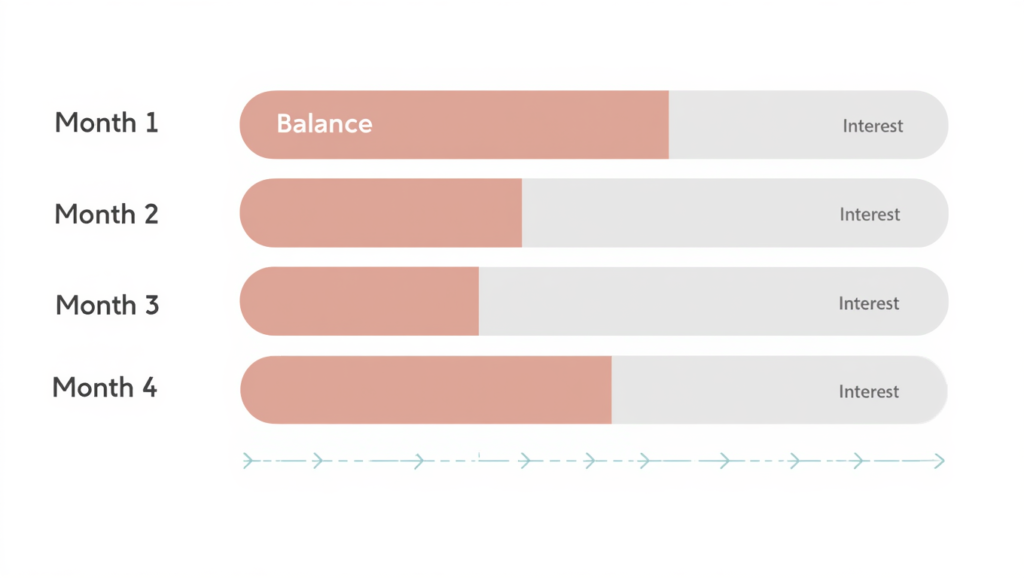

Why Minimum Payments Keep You Stuck in Debt

Minimum payments are calculated to protect the lender, not the borrower.

Because interest is charged daily:

- A large portion of each payment covers interest

- The balance reduces at a slow pace

- Progress feels invisible

Over time, this can create a false sense of control. You are paying regularly, but the debt is barely moving.

This is how long-term credit card debt often forms without any dramatic spending mistakes.

How Long Does It Take to Clear a Balance With Minimum Payments?

This depends on the balance and interest rate, but the pattern is consistent.

For example:

- A balance of £2,000

- Typical UK credit card interest rate

- Minimum payments only

It can take many years to clear the balance and cost significantly more in interest than the original spending.

This is why minimum payments should be seen as a safety net, not a strategy.

How Minimum Payments Affect Your Budget

When you only pay the minimum:

- Monthly payments stay low at first

- Interest keeps balances high

- Budgets feel tight for longer

- Credit card spending feels permanent

This often leads people to feel that credit cards ruin budgets. In reality, the issue is not the card, but the repayment approach.

This relationship is explored further in Are Credit Cards Bad for Budgeting?

Does Paying the Minimum Hurt Your Credit Score?

Paying the minimum does not damage your credit score directly, as long as payments are made on time.

However, indirect effects matter:

- Balances stay high

- Credit card utilisation remains elevated

- Lenders may see higher risk

Over time, this can limit credit improvement even with perfect payment history.

For a deeper explanation of this, see Credit Card Utilisation Explained (UK).

When Paying the Minimum Might Be Necessary

There are times when paying the minimum is unavoidable.

This may happen if:

- Income drops temporarily

- Unexpected costs arise

- You are prioritising essentials

Paying the minimum is better than missing a payment. The key is not letting it become the default long-term habit.

What to Do Instead of Only Paying the Minimum

If you want to get out of the minimum payment cycle, small changes matter.

Better approaches include:

- Paying more than the minimum whenever possible

- Making mid-month payments to reduce interest

- Focusing extra money on one balance at a time

- Avoiding new spending while paying down debt

You do not need perfection. Even modest overpayments can shorten repayment time significantly.

How This Fits Into Responsible Credit Card Use

Minimum payments are part of the system, but they are not designed to help you become debt-free.

Families who stay in control of credit usually:

- Use cards intentionally

- Track balances regularly

- Aim to pay in full where possible

- Reduce reliance on minimum payments over time

These principles sit within the wider framework explained in Credit Cards and Debt Explained for UK Families.

Frequently Asked Questions About Paying the Minimum on a Credit Card

Is it bad to only pay the minimum on a credit card?

Paying the minimum is not technically wrong, and it keeps your account in good standing. However, it is usually the most expensive way to repay debt.

Minimum payments mostly cover interest rather than the balance itself. This means the debt reduces very slowly, and you can end up paying far more than the original purchase.

Does paying the minimum hurt your credit score?

Paying at least the minimum does not harm your credit score directly, because you are meeting the lender’s required payment.

However, if your balance stays high compared to your credit limit, it can increase your credit utilisation ratio, which may negatively affect your score over time.

How long does it take to clear a credit card if you only pay the minimum?

It can take many years.

For example, a £2,000 balance at typical credit card interest rates could take over a decade to repay if only minimum payments are made. During that time, the total interest paid can exceed the original debt.

This is why lenders are now required to warn customers when repayment could take too long.

Why do credit card companies allow minimum payments?

Minimum payments are designed to make the debt manageable in the short term. They prevent accounts from immediately falling into default.

However, the structure also means balances can last much longer, which increases the interest lenders receive.

Is paying slightly more than the minimum better?

Yes. Even a small increase in your monthly payment can significantly reduce the time it takes to clear the balance.

For example, paying £20 more each month can shorten repayment by years and reduce the total interest paid.

What happens if I miss the minimum payment?

If you miss the minimum payment, several things may happen:

• Late payment fees may be added

• Interest can increase

• Your credit report may record a missed payment

• Your credit score may drop

Multiple missed payments can lead to more serious consequences such as default notices.

Should I stop using my credit card while paying off debt?

In most cases, yes. Continuing to spend on the card while trying to repay the balance often slows down progress.

Many people find it easier to clear debt by pausing new spending and focusing on repayment first.

Is paying the minimum ever the right choice?

Sometimes it can be a temporary strategy during financial pressure.

If money is tight, paying the minimum keeps the account active and avoids missed payments. The key is to treat it as a short-term solution rather than a long-term habit.

What is the best strategy to pay off credit card debt faster?

Common strategies include:

• Paying more than the minimum each month

• Prioritising the card with the highest interest rate

• Using the debt snowball or debt avalanche method

• Avoiding new spending on the card

The most effective approach is the one that fits your budget and keeps you consistent.

Final Thoughts

If you are asking “what happens if you only pay the minimum credit card payment”, the honest answer is this:

You stay in debt longer, pay more in interest, and feel the impact on your budget for years.

If you want to get out of debt faster, explore these proven debt repayment strategies to crush your debt.

Minimum payments protect your account, not your finances. They are a short-term tool, not a long-term plan.

Understanding this gives you the power to change direction, even gradually.

For a complete overview of how credit cards, repayments, and budgeting work together, read Credit Cards and Debt Explained for UK Families.

Understanding this behaviour is key to using credit cards responsibly. This topic is covered more broadly in the Credit Cards and Debt pillar page, where you can see how minimum payments fit into the bigger picture.

Related Credit Card Guides

If you are working to improve your finances, these guides can also help:

• Learn what really happens when you only pay the minimum on a credit card

https://budgetkin.com/paying-the-minimum-on-a-credit-card-what-really-happens-in-the-uk/

• Understand how credit card utilisation affects your credit score

https://budgetkin.com/credit-card-utilisation-explained-and-why-it-matters-in-the-uk/

• Avoid credit card mistakes that hurt your finances

https://budgetkin.com/credit-card-mistakes-that-hurt-your-finances/

• Explore proven debt repayment strategies to crush your debt

https://budgetkin.com/proven-debt-repayment-strategies-to-crush-your-debt/

Pingback: 10 Proven Debt Repayment Strategies to Crush Your Debt - BudgetKin

Pingback: Credit Card Mistakes That Hurt Your Credit Score in the UK - BudgetKin

Pingback: Credit Card Utilisation Explained (And Why It Matters in the UK) - BudgetKin

Pingback: How Many Credit Cards Should I Have in the UK? - BudgetKin